Categories

investment, HomeownershipPublished June 12, 2026

Mortgage 101

Understanding Mortgage & Financing Basics: A Guide for Homebuyers

Purchasing a home is one of the most significant financial decisions many of us will make. Navigating the world of mortgages and financing can seem daunting at first, but with a clear understanding of the basics, you can approach the process with confidence and optimism. Here’s a straightforward guide to help you get started on your homebuying journey.

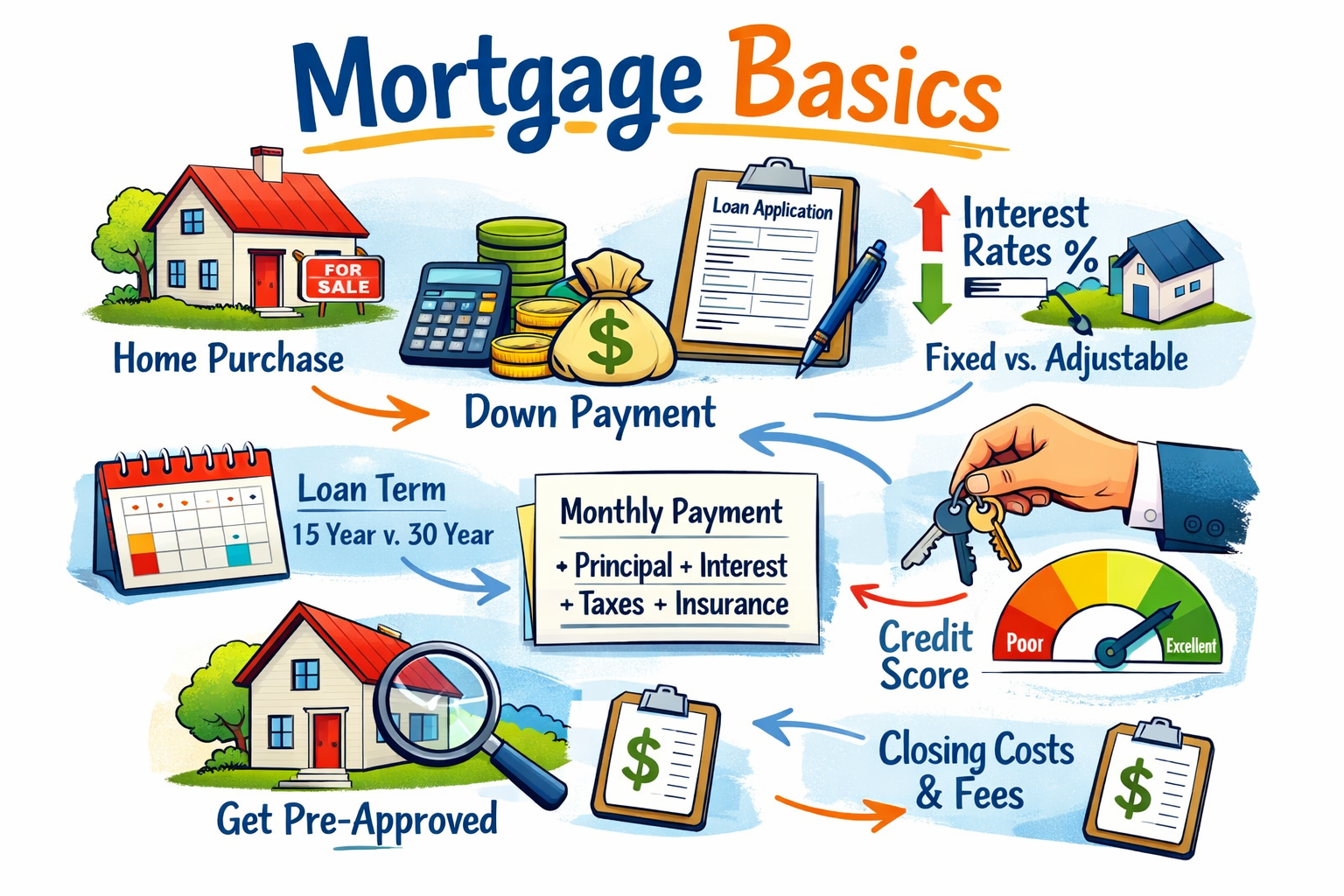

What Is a Mortgage?

A mortgage is a loan specifically designed to help you buy a home. Instead of paying the full price upfront, you borrow money from a lender and agree to pay it back over time, typically with interest. The home itself serves as collateral, meaning if you don’t keep up with payments, the lender can take ownership of the property.

Types of Mortgages

-

Fixed-Rate Mortgage: This is the most common type, where your interest rate stays the same throughout the loan term, usually 15 or 30 years. It offers stability and predictable monthly payments.

-

Adjustable-Rate Mortgage (ARM): The interest rate starts lower than a fixed-rate mortgage but can change periodically based on market conditions. This option might be suitable if you plan to sell or refinance before the rate adjusts.

-

FHA Loans: Backed by the Federal Housing Administration, these loans are designed for buyers with lower credit scores or smaller down payments.

-

VA Loans: Available to veterans and active military members, these loans often require no down payment and offer competitive rates.

Key Financing Terms to Know

-

Down Payment: The upfront amount you pay toward the home’s purchase price. While 20% is traditional, many loans allow for lower down payments.

-

Interest Rate: The cost of borrowing money, expressed as a percentage. Lower rates mean lower monthly payments.

-

Loan Term: The length of time you have to repay the loan, commonly 15 or 30 years.

-

Private Mortgage Insurance (PMI): If your down payment is less than 20%, lenders may require PMI, which protects them if you default.

Steps to Secure Financing

-

Check Your Credit Score: A higher score can help you qualify for better rates.

-

Get Pre-Approved: This involves a lender reviewing your financial information to determine how much you can borrow, giving you a clear budget and strengthening your offer.

-

Shop Around: Compare rates and terms from multiple lenders to find the best fit.

-

Understand Closing Costs: These are fees associated with finalizing the loan, typically 2-5% of the purchase price.

Why Work with a Trusted Realtor?

Having a knowledgeable real estate professional by your side can make all the difference. Someone like Cole Rakes from Story House Real Estate brings not only expertise in the local market but also a deep commitment to guiding clients through every step of the transaction. From coordinating with lenders to ensuring a smooth closing, a trusted realtor helps turn the complex process into a manageable and even enjoyable experience.

Final Thoughts

Mortgage and financing may seem complex, but with the right information and support, you can confidently move forward toward homeownership. Remember, every buyer’s situation is unique, so take the time to explore your options and ask questions. Your dream home is within reach, and understanding these basics is the first step to making it yours.

|

or another way